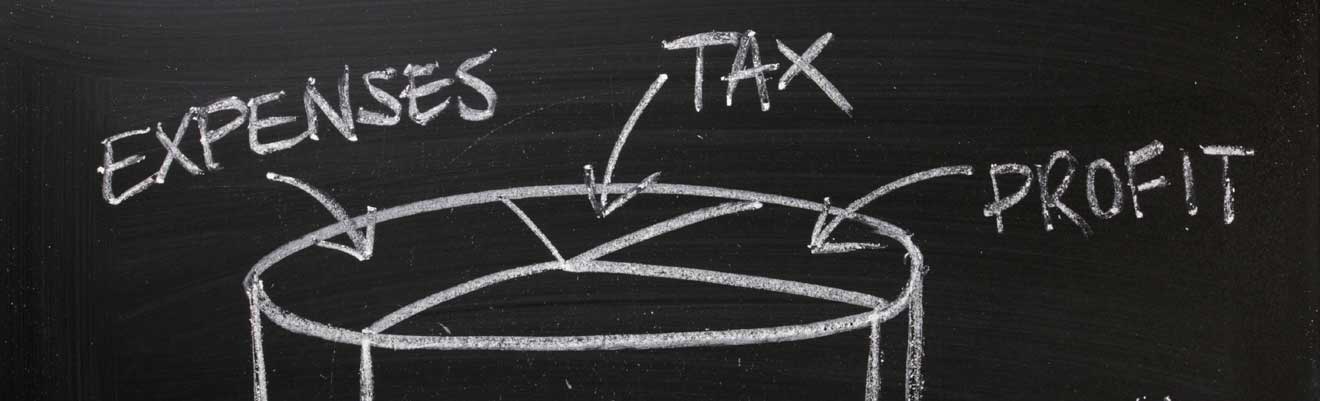

Income Tax & Capital Gains Tax

Income tax rates and capital gains tax rates have increased.

In addition, clients must also pay the 3.8% Affordable Care Tax. This substantial increase in income tax rates has made income and capital gains tax planning more compelling and relevant than ever before.

We are tax lawyers based in Little Rock, Arkansas

However, we are aware that tax planning opportunities are not limited by state or national borders. Some of the most effective tax planning solutions are found in other states or in the U. S. territories.

Solutions

We provide our clients a unique set of solutions that can, in the right situations, significantly reduce the impact of the Income Tax and the Capital Gains Tax.

- Tennessee & Alaska Community Property Trusts

- Puerto Rico and U. S. Virgin Islands Tax Benefit Programs

- DING/NING Trusts

- Private Placement Life Insurance

- Charitable Remainder Trusts

- Captive Casualty Insurance Company Planning

- Basis Step-Up Planning

Captive Casualty Insurance

A captive insurance company, typically referred to as a “captive,” is an insurance company that you own. It’s a risk management insurance structure that, when set up and operated in compliance with state regulations and IRS guidelines, can provide substantial risk mitigation, economic, tax, and estate planning benefits.

CLICK HERE TO LEARN MORE

A captive issues policies that protect you against business risks for which coverage from commercial insurance carriers may be unavailable or unaffordable. Instead of paying premiums to a commercial insurance carrier, you pay premiums for coverage to your captive company. Any unused premiums your business pays accrue to your benefit as equity in the captive instead of going out the door to a carrier. The premiums paid to the captive may qualify as deductible for the business or professional practice.

Why Consider A Captive?

- A captive can redirect current cash flow into your own insurance company to provide protection against business risks while simultaneously building shareholder equity.

- A captive can protect you against business risks for which coverage from commercial insurance carriers is unavailable or unaffordable.

- Unlike with a traditional insurance carrier, any unused premiums your business pays accrue to your benefit as equity in the captive—not profits to the owners of a commercial insurance company—thereby potentially increasing your overall business income.

- The premiums paid to the captive may qualify as deductible for the business or professional practice.

- It has the potential to accumulate wealth in the form of premium reserves on a tax-advantaged basis.

- Subject to reserve requirements, the owner controls the captive’s equity and premium reserves in a financial institution and permitted investments that he or she selects.

- Equity in the captive may be available for distribution to the owner as dividends, subject to reserve requirements, or upon liquidation as capital gains.

- Subject to certain restrictions, profit distributions can occur at the owner’s discretion.

- Captive insurance companies are, first and foremost, an effective risk management tool for successful business owners and professionals. Under appropriate circumstances, ownership of a captive can also play an important role in financial and estate planning, especially for family-owned businesses.

- Captives can be owned by LLCs, partnerships, corporations, trusts, key employees, family members, and individuals, thus adding potential benefits beyond risk management, including asset protection, wealth preservation, and maximizing the transfer of wealth to heirs.

The IRS Is Examining Captives Closely Now

The IRS is taking a hard look at captive insurance companies and the managers of captive insurance companies.

In audits, the IRS is focusing on several questions:

- Why was the captive created? How did the captive manager market to the captive owner?

- Do the premiums look managed to a tax outcome? That is, do annual premiums vary in tandem with the business’s taxable income for the year, or conversely, do premiums hover at or near the $1.2 million mark year in and year out?

- Were there any claims made against policies? And were there claims made against the risk pool that is often a part of the small captive setup?

- Do coverages appear warranted and do premiums appear correctly calculated? Do the premiums vary by reason of underwriting on an annual basis?

- Who owns the captive? Is it held in trust for the benefit of others or future generations?

- What kinds of investments are present? Has life insurance been purchased?

We Can Help

While the captive solution can provide compelling benefits, the increased level of scrutiny does underscore the need to make certain your captive is properly established and properly operated. We can help you develop your captive insurance strategy that will comply with IRS requirements.

More Solutions Are Available From Our Consulting Affiliate

Our consulting affiliate ILP + Business Solutions, LLC and its network of affiliate partners provide a broad range of consulting services that can reduce the tax burden of successful businesses and entrepreneurs. Generally, the fees paid to our consulting company are entirely contingent on the results the business produces for the client. ILP + Business Solutions, LLC provides a wide range of tax related services, including:

For more information on the services ILP + Business Solutions, LLC provides, click here:

The Virgin Islands & Puerto Rico Tax Benefit Programs

The government of the United States Virgin Islands and the government of Puerto Rico provide generous tax benefits for qualified business activities that are accepted into those programs. Businesses interested in relocating to the USVI or Puerto Rico can achieve up to a 90% reduction in their income tax burden for qualified business activities. These programs are ideal for businesses that are not location-dependent. There are several requirements including a residency requirement.

Puerto Rico also has a program that totally eliminates the capital gains tax on all gain that accrues after the individual relocates to Puerto Rico.

Our staff will guide you through the application process and then help you manage the complex rules that govern the businesses that participate in these programs.Our professional staff understands the policy behind the laws that permit significant tax credits designed to support economic growth in our nation’s territories. As government employees, we regulated these programs. As private attorneys, we have drafted many of the laws that enhance these tax advantaged programs.

Our firm brings a unique experience set to our representation of major resort developments in the Caribbean. Mr. McChain, who holds a CPA license, has a prior history of auditing large scale commercial entities and non-profit organizations. Mr. Nissman was a CEO of a major lending and development company prior to entering the private practice of law. Their varied business backgrounds provide practical insight and added value to their business clients.

Alaska & Tennessee Community Property Trusts

This is a very interesting solution for our clients who are married and who own appreciated assets. Couples who live in a “Community Property” jurisdiction enjoy a distinct advantage over couples who live in so-called “Common Law” jurisdictions. The Community Property jurisdictions include Louisiana, Texas, New Mexico, Arizona, Nevada, California, Idaho, Washington and Wisconsin. The other 41 states are Common Law jurisdictions.

The benefit to the Community Property jurisdictions is that when one spouse dies, the entire value of the couple’s community property receives a “step-up” in cost basis—thus allowing the asset to be sold without incurring any state or federal capital gains tax on the pre-death appreciation. In a Common Law jurisdiction, only one-half of the couple’s assets would receive this step-up in basis.

In 1998 Alaska adopted a unique community property statute that allows non-Alaska residents in separate property states to take advantage of federal income tax laws that favor community property. Effective July 1, 2010, the Tennessee legislature cloned the Alaska legislation. Trusts created to take advantage of these laws can translate into substantial capital gains tax savings, with few downside risks.

Here is generally how it works. IRC §1014(b)(6) allows an adjustment (usually a step-up) to basis on property which represents the surviving spouse’s one-half share of community property held by the decedent and the surviving spouse under the community property laws of any state, or possession of the United States or any foreign country, if at least one-half of the whole of the community interest in such property was includable in the value of the decedent’s gross estate.

Alaska, and now Tennessee law allows married residents of separate property states (such as Arkansas) to elect community property treatment for some or all of their property by establishing an Alaska Revocable Community Property Trust or a Tennessee Revocable Community Property Trust. Typically, the trust is structured to split and “pour back” into the clients’ revocable trust when the first spouse dies. Because trust assets are classified as community property under Alaska or Tennessee law, IRC § 1014(b)(6) provides a “full adjustment” in basis to date of death values at the death of the first spouse.

This technique can be very powerful for our clients who have a substantial amount of appreciated property (including stocks, real estate and closely held business interests) because the 100% basis step-up at the first death will allow the asset to be sold after the first death—regardless of which spouse dies first. There are a few requirements that must be met in order to establish these trusts, but these requirements are easily satisfied.

Our Connections

ILP + The Book

It is possible to protect yourself, your family and your business or professional practice from the real threats that keep you up at night. The law provides more and better solutions than ever before in history. In this book, Stan explains in clear, understandable language how these powerful solutions can be deployed to protect what you have earned and built.

Available Early Summer 2015

ILP + The Webinar

In this hour-long webinar, Stan explains how to avoid probate and protect your heirs with a revocable living trust. You will learn how to protect your loved ones what many consider to be an expensive, lengthy, and unnecessary court process. You will also learn what a living trust is and why having a living trust will protect your children, grandchildren and other heirs.

Available Now

Numbers Don’t Lie

0

Years of Combined Experience

0

In Billions, the Dollar Value of Wealth We Have Protected

0

The Number of Clients We've Served

0

The Percentage of Clients Who Say They Will Refer Their Friends To Us